管理会计第三章 本量利分析(management accounting; the third chapter; quantitative analysis of profit and loss) 14页

- 39.50 KB

- 2022-05-14 14:48:59 发布

管理会计第三章 本量利分析(management accounting; the third chapter; quantitative analysis of profit and loss)

- 1、本文档共5页,可阅读全部内容。

- 2、本文档内容版权归属内容提供方,所产生的收益全部归内容提供方所有。如果您对本文有版权争议,可选择认领,认领后既往收益都归您。

- 3、本文档由用户上传,本站不保证质量和数量令人满意,可能有诸多瑕疵,付费之前,请仔细先通过免费阅读内容等途径辨别内容交易风险。如存在严重挂羊头卖狗肉之情形,可联系本站下载客服投诉处理。

- 文档侵权举报电话:19940600175。

管理会计第三章本量利分析(Managementaccounting;thethirdchapter;quantitativeanalysisofprofitandloss)Thischapterfocuseson:1、profitandlosscriticalpointanditscalculation.2,thevolumeofprofitrelationsdiagram.3.Correlationfactorbreakevenanalysis.4,sensitivityanalysisofrelatedfactors.ThefirstcostvolumeprofitanalysisFirst,theconnotationofquantitativeandprofitanalysisCVPanalysisisanabbreviationofbetweencost,businessvolume,profitthreedependencyrelationanalysis,isbasedoncostofstatedivisionandthechangecostmethod,accountingmodelandschemabymathematicaltorevealtheregularityofthechangeoffixedcost,relationshipbetweencostandprice,salesvolume,salesandprofitvariables,aquantitativeanalysismethodforaccountingforecasting,decision-makingandplanningtoprovidethenecessaryfinancialinformation.Two,thepremiseofquantitativeandquantitativeanalysis:1,costbehavioranalysishypothesis;(allcostscanbedividedintotwoparts:fixedandvariable)

2,therelatedrangeandlinearhypothesis;(timeandspacearelimited,costsarelinearlyrelatedtovolumeofbusiness)3,thebalanceofproductionandmarketingandthehypothesisofstablevarietystructure;(outputequalssales,andtheproportionofproductsvariessteadily)4,variablecostinghypothesis;(coststructureandprofitcalculationprocedure)5,targetprofithypothesis.(operatingprofit)Three,basicrelationsandrelatedindicators1,basicformula:Operatingprofit=operatingincome-totalcostP=px-(a+bx).EmphasizesthetotalamountofrelationsamongvariousfactorsP=(px-bx)-a?.?emphasisoncontributionmarginindicatorsP=(P-B)x-a

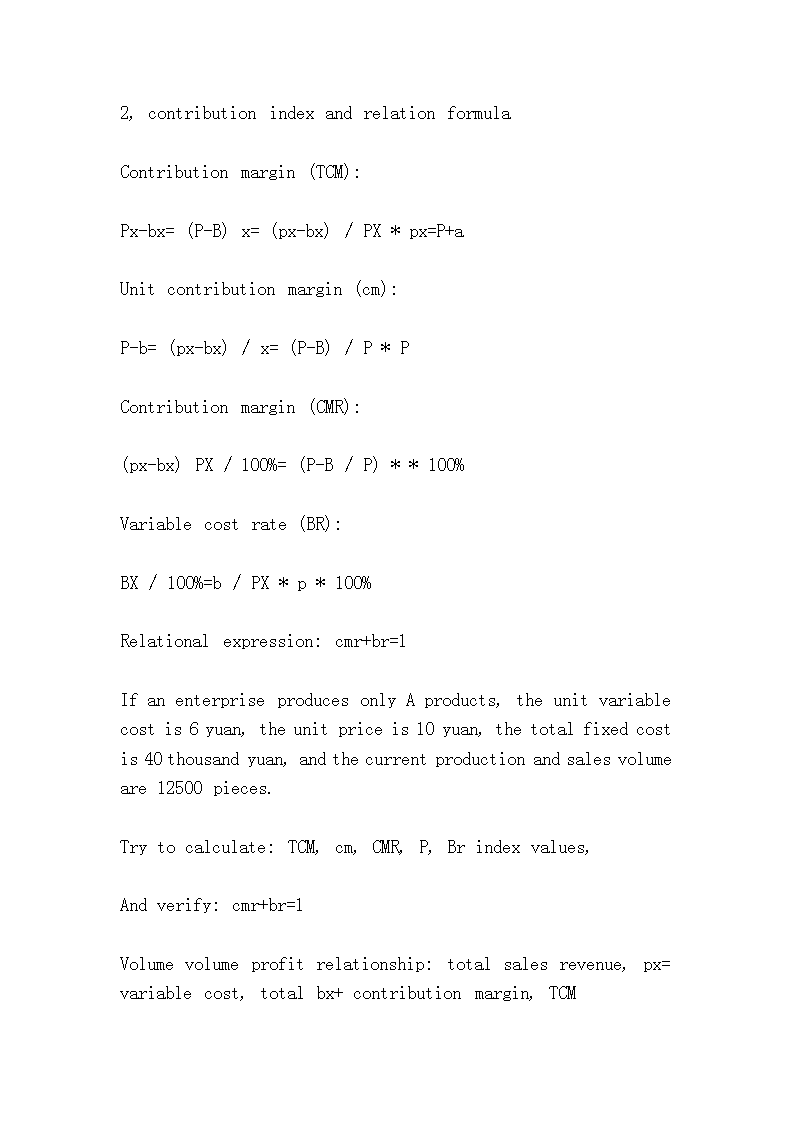

2,contributionindexandrelationformulaContributionmargin(TCM):Px-bx=(P-B)x=(px-bx)/PX*px=P+aUnitcontributionmargin(cm):P-b=(px-bx)/x=(P-B)/P*PContributionmargin(CMR):(px-bx)PX/100%=(P-B/P)**100%Variablecostrate(BR):BX/100%=b/PX*p*100%Relationalexpression:cmr+br=1IfanenterpriseproducesonlyAproducts,theunitvariablecostis6yuan,theunitpriceis10yuan,thetotalfixedcostis40thousandyuan,andthecurrentproductionandsalesvolumeare12500pieces.Trytocalculate:TCM,cm,CMR,P,Brindexvalues,Andverify:cmr+br=1Volumevolumeprofitrelationship:totalsalesrevenue,px=variablecost,totalbx+contributionmargin,TCM

(contributionmargin=fixedcost,a+profit,P)Fillintheblanksintheanswer:Titlenumber,salesvolume,x,salesrevenue,PX,variablecost,BXcm,fixedcost,aprofit,P5000041000010000II8000400003900030004500018000-3000900081000450002000SecondcostvolumeprofitanalysisFirst,avarietyofcapitalpreservationanalysis1.breakevenanalysisBreakevenanalysisistostudytheprofitandlossrelationshipinwhichtheenterpriseisjustinthestateofbalanceofpayments,lossofprofitandloss,andzeroprofit.Breakevenpoint(BEP):thebusinesspointthatenablestheenterprisetoreachitsbreakevenstate;Therearetwospecificformsofperformance:breakevenpoint,salesvolume,yandbreakevenpointsales.

2,themethodofdeterminingthesinglebreakevenpoint:Basicformulamethod:definitionmethodPXo-(a+bXo)=0orpXo-bXo=aGet:PaulXo=a/volume(P-B)BreakevenamountYo=p*xContributionmarginmethod:ThisamountofXo=a/cmThisamountofYo=a/CMRGraphicalmethod:usethebreakevendiagramtodeterminethesizeofthebreakevenpoint.Example:anenterpriseoperatesaproduct,thenormalmonthlysalesvolumeis4000pieces,thesellingpriceis25yuan,theunitvariablecostis15yuan,thefixedcostis25000yuan.Calculatebreakevenvalue.3,safetymarginindex(marginofsafety)Themarginofsafetyisthequantitativeindexthattheactual(expected)valueexceedstheguaranteedvalue,andtherearethreespecificformsofitsperformance:themarginofsafety,themarginofsafetyandthemarginalrateofsafety.

Marginofsafety(MSu)=actualquantity-guaranteedcost=X-XoMarginofsafety(MSd)=actualamount=Y-YoSafetymarginrate(MSR)=(theactualamount-guaranteedamount),X=(X-Xo)/X(Y-Yo/Y)*100%=*100%Note:safetymargin=marginalcontributionThemarginofcontributionprovidedbythemarginofsecurityisprofit.MSd*cmr=P;MSu*cm=PEnterprisesafetymanagementstandardMSR10%,11-20%,21-30%,31-40%,41%ormoreSafetyisdangerous.Itisworthnotingthatitissafer,saferandsaferAnalyzethefollowingsafetymarginindexvalues,dotheyexist?Whatdotheymean?Whataretherules?-200%;-100%;0;30%;80%;100%;200%Breakevenoperationindex

Thebreakevenoperationrateisalsocalledriskrate(DR),whichmeansthatthepercentageoffixedpointtrafficaccountsforcurrentorprojectedsalesisarelativeinversemeasure.Dr=breakevenvalue/actualvalue=Xo/x=Yo/y*100%Rangeofvalues:(0++)-cannotbenegative.100%--breakeven;>100%--loss;<100%--earnings;Relationalformula(proofprocess)Marginofsafety(MSR)+guaranteedoperatingratio(DR)=1;Breakevenvalue=actualvalue*(1-marginofsafety);Targetprofit=fixedcost*safetymargin/breakevenvalue;Profit=unitcontributionmargin*safetymarginNamely:P=cm*MSu=(P-B)*(X-Xo);Salesmargin=marginofsafety*contributionmargin;Added:targetprofit,polypoint.Qualitativeanalysisofthesensitivityofbreakevenpoint(polypoint):

WhenthepriceisupP:guaranteedvalue:Value:value=polysafetymarginWhenB=:guaranteedvalue=value=marginofsafety:PolyWhena=:guaranteedvalue=value=marginofsafety:PolyWhenthetargetis:Po=profitguaranteedvalue,polyvalueincreaseMarginalvalueofsafety;Whenx=sales:guaranteedvalue,polyvalue,safetymarginvalueincreaseStandardprofitandlosscriticaldiagram:breakevenpointunchanged,thegreaterthesales,themoreprofits,thebreakpointpositionbyP,a,Bimpact,notaffectedbytheX.Contributionbreakevenchart:incomestatementformationprocess,incomevariablecosts-fixedcosts;TCMa-earnings;WiththeincreaseinsalesofX:fromlosstoguaranteetoprofitQuantitativecriticalgraphs:profits=cm*MSu=cm*(x-X0);Theslopeoftheprofitlineiscm;profitisproportionaltosales.Two,manyvarietiesofproductsguaranteedanalysis

1,comprehensivecontributionmarginmethodBycalculatingthecomprehensivecontributionmargin(cmR"),thecommonburdenoffixedcosts,theproportionoftotalcapitalpreservation,andthengettheproduct"sguaranteedvalue.Guaranteedtotal=totalfixedcostdividedbycmR"factoryThekeyofthismethodishowtocalculatethevalueof"cmR"correctly.Themainmethodsare:thesummethodandtheweightedaveragemethodTotalmethod:Basedonthedefinitionofcontributionmargin,thetotalcontributionmarginofthewholeplantisdeterminedbytheratioofthetotalamountofsalestothetotalsalesrevenue.CmR"=SigmaCMX/sigmaPX*100%Examples:anenterpriseorganizationABCthreeproductsintheproductionandoperationofthewholeyearisexpectedtototalfixedcostof300thousandyuan,saleswere100thousand,25thousand,10thousand;10,20,price:50yuan;thevariablecostperunit:8.5,16,25yuan;calculationamountandguaranteedtoachieve150thousandyuanofprofitssales.Solution:cmR"=500000/2000000=25%Thetotalamountof=a/cmRguaranteedfactory"=120million

yuanTheamountofpoly(a+P)/cmR"==180yuanTheguaranteedvalueofindividualproductscanbefurtherdistributedaccordingtothesalesproportion.Weightedaveragemethod:onthebasisofcalculatingthecontributionmargincmRiofeachproduct,theweightedaverageofthesalesproportionistakenastheweighttocalculatethe"cmR"Thatis,"cmR"=SigmacmRi*BiFollowtheabovedata,threekindsofproductsofcmRiandBirespectively:15%,20%,50%and50%,25%,25%;ThencmR"=15%*50%+,20%*25%+50%*25%=7.5%+5%+12.5%=25%L=300000/25%=1200000yuantotalguaranteedAproductguaranteeamount=120x50%=60yuanBproductguaranteeamount=120x25%=30yuanCproductguaranteeamount=120x25%=30yuan2,jointunitlaw:todeterminetheproportionofthestablestructureofeachproductasajointunit,thejointunitas

anindependentunitofcalculation,tocarryoutthecapitalpreservationanalysis.Itsspecificsteps:Determinethejointunit(usuallyinproportiontothesalesoftheproduct);Calculatejointunitprice;Calculatethevariablecostofjointunit;Calculatecombinedguaranteedcost;Determinetheguaranteedamountofeachproductinproportion;Thecalculationoftheamountofcapitalpreservationproducts.Usingtheabovedata,thecombinedunitbody:A:B:C=10:2.5:1;Unionunitprice=10*10+20*2.5+50*1=200yuan;Combinedvariablecost=8.5*10+16*2.5+50*1=150yuanTheamountof=300000/jointpreservation(200-150)=6000XA=10*6000=60000pieces;YA=600000yuanXB=2.5*6000=15000platform;YB=300000yuanXC=1*6000=6000sets;YC=300000yuan.

ThirdcostvolumeprofitanalysisextensionFirstly,thecostfactoranalysisundernonlinearconditions1,determinethecriticalpointofprofitandloss-usethedefinitiontoobtain.Multiplecriticalpointsmayoccur.P782,usethemarginalindextogetthemaximumprofit.Marginalrevenue=marginalcost,ormarginalprofit=03,calculatetheoptimalprice,thatis,themaximumprofitundertheprice.Two.ThemethodofquantityprofitanalysisunderuncertaintyMethod1:theexpectedvaluesofunitprice,unitvariablecostandfixedcostarecalculatedaccordingtoprobability,andthentheformulaisderived.Example:thedataforeachfactorisshowninthetablebelow:Unitprice;variablecost;fixedcostHorizontalprobability;horizontalprobability;horizontalprobabilityMaybe1,210.315,0.215600,0.4

Probably200.616,0.815000,0.6Possible190.1Trytocalculatethebreakevenamounttoachievethetargetprofitmarginof11400yuanandtheexpectedprofitwhenthesalesvolumeis6000.Unitpriceexpectation=21*0.3+20*0.6+19*0.1=20.2Theexpectedvalueof=15isb*0.2+16*0.8=15.8Theexpectedvalueof=15600isa*0.4+15000*0.6=15240Theamountof=15240/Lguaranteed(20.2-15.8)=3464Achieve11400targetprofitsales:(15240+11400)/(20.2-15.8)=6055Whenthesalesvolumeis6000,theexpectedprofitis:(20.2-15.8)*6000-15240=11160Or:(20.2-15.8)*(6000-3464)=11160Methodtwo:calculatetherelativeindexandjointprobabilityofdifferentcombinations,andmakeweightedaverage.Thecalculationisrelativelycomplicated.

Usingtheabovedatacalculationresults:Xo=3561;X2=5802;P=11160;Slightlydifferentfrommethodone.